Climate change is reshaping the global economy, affecting production in industries that are highly dependent on natural resources and changing consumer demands. As countries aim to curb greenhouse gas (GHG) emissions and consumers seek more sustainable products and services, demand is shifting away from high-emission industries toward more sustainable alternatives. Global investors are recognising this opportunity: Sustainable funds attracted a record US$69.2bn in net flows in 2021, a 35% increase over 2020, when the previous record was set.1

However, investors have yet to fully recognise the opportunity presented by the net-zero transition in Latin America. Currently, the region only contributes to 2% of global green bond issuance.2

With immense natural capital and a growing urban population, Latin America stands to become a crucial player in the green economy. From sustainable agriculture to clean energy and transport, investment in low-emission industries and ecosystem services can become an avenue of long-term growth for Latin American investors. This article explores how the demand for low-carbon alternatives is creating investment opportunities in some of Latin America’s key economic sectors, which also capitalise on the region’s unique natural assets. Our research found that:

- The net-zero transition could reduce the estimated oil and gas production by 2050, as reduced dependency on fossil fuels accelerates the adoption of renewable energies.

- Issuance of green bonds in Latin America more than doubled in the last two years and is helping finance renewable energy, transportation and land-use projects.

- Investment in agricultural technologies and sustainable practices could help the sector adapt to shifting demands by enhancing crop yields, address food waste and improve livestock farming.

- The Amazon Basin, one of the few carbon sinks in the world, contributes to the region’s vast carbon sequestration potential, positioning it as a leader in the voluntary carbon credit markets.

Shifts in Demand and Geopolitical Risks in Energy Markets Create Opportunities for Renewables Energy

To limit climate change’s impacts, countries must pursue net-zero emissions, balancing the amount of GHGs produced and removed. Achieving net-zero will require countries to shift demand from carbon-intensive operations to lower-emission alternatives. In the energy sector, which is currently the source of 46% of Latin American emissions, this would require relying less on fossil fuels and increasing demand for renewable electricity generation, hydrogen and biofuels.3,4

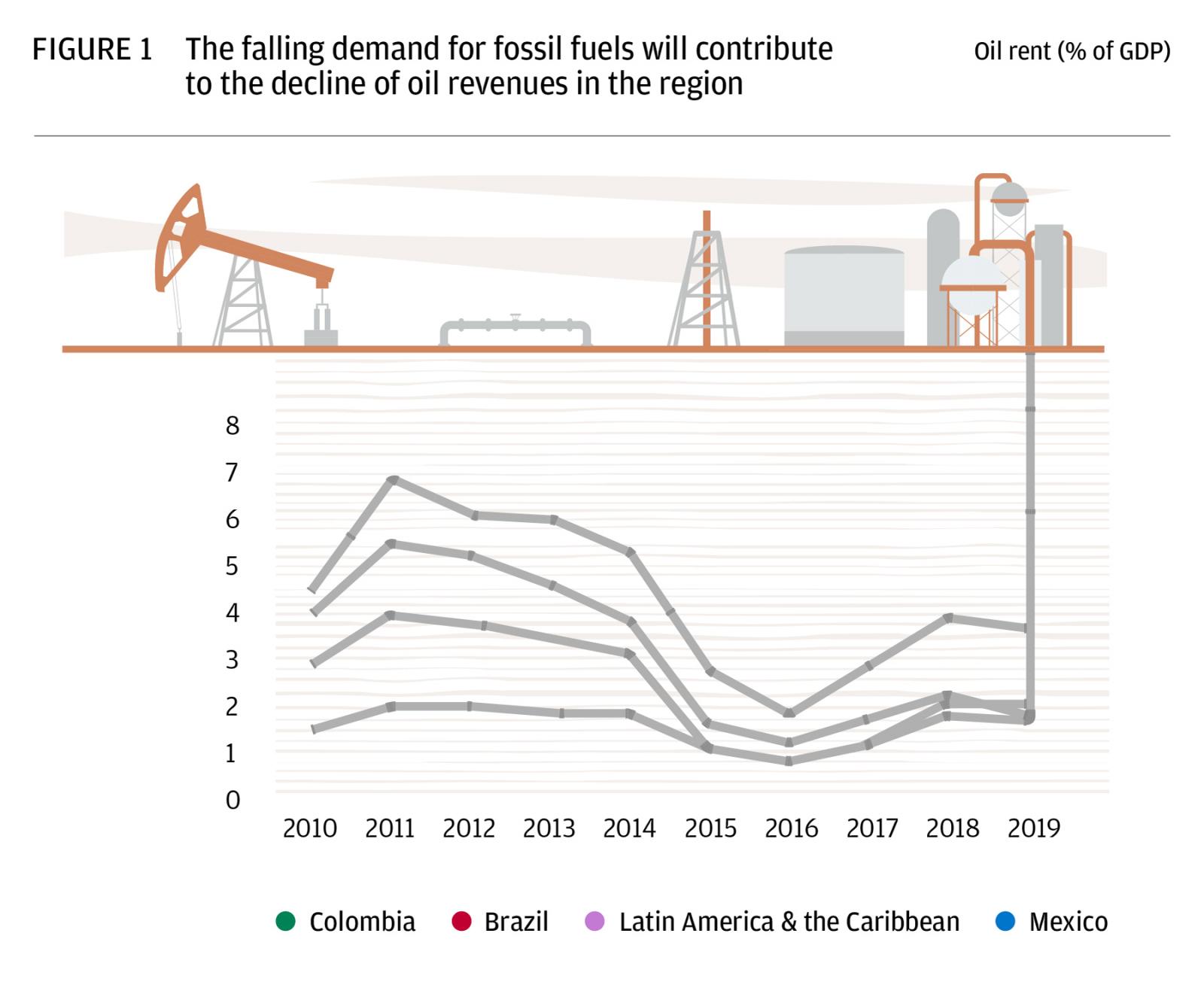

This shift would challenge the oil and gas industry, which historically has contributed a significant percentage of the region’s GDP. Estimates suggest that by 2050, oil and gas production volumes could be 55% and 70% lower than today.5 The region has already seen a steady decline in revenue from oil over the past decade. On average, oil rent6 in Latin America represents 1.7% of GDP compared with 3% in 2010. For countries such as Mexico, revenue from oil has more than halved in the past 10 years (see Figure 1).

The sharp increase of oil and gas prices and the mounting geopolitical risks associated with dependency on fossil fuels could accelerate renewable energy adoption. Amid stock losses because of Russia’s invasion of Ukraine, renewables are outperforming, as power prices jump and investors seek energy alternatives.8 As industries phase out fossil fuels, Latin America will have to undergo an energy transformation. This shift will require sizable investments in renewable and clean energy sources, representing a long-term opportunity for investors.

Issuance of Green Bonds in Latin America has More than Doubled in Two Years, Enabling the Region’s Net-Zero Transition

Putting a number to this transformation, the International Finance Corporation (IFC) estimates that the cumulative investment opportunity for renewable energy infrastructure in the region amounts to US$555bn by 2030, more than 12% of the region’s current GDP.9

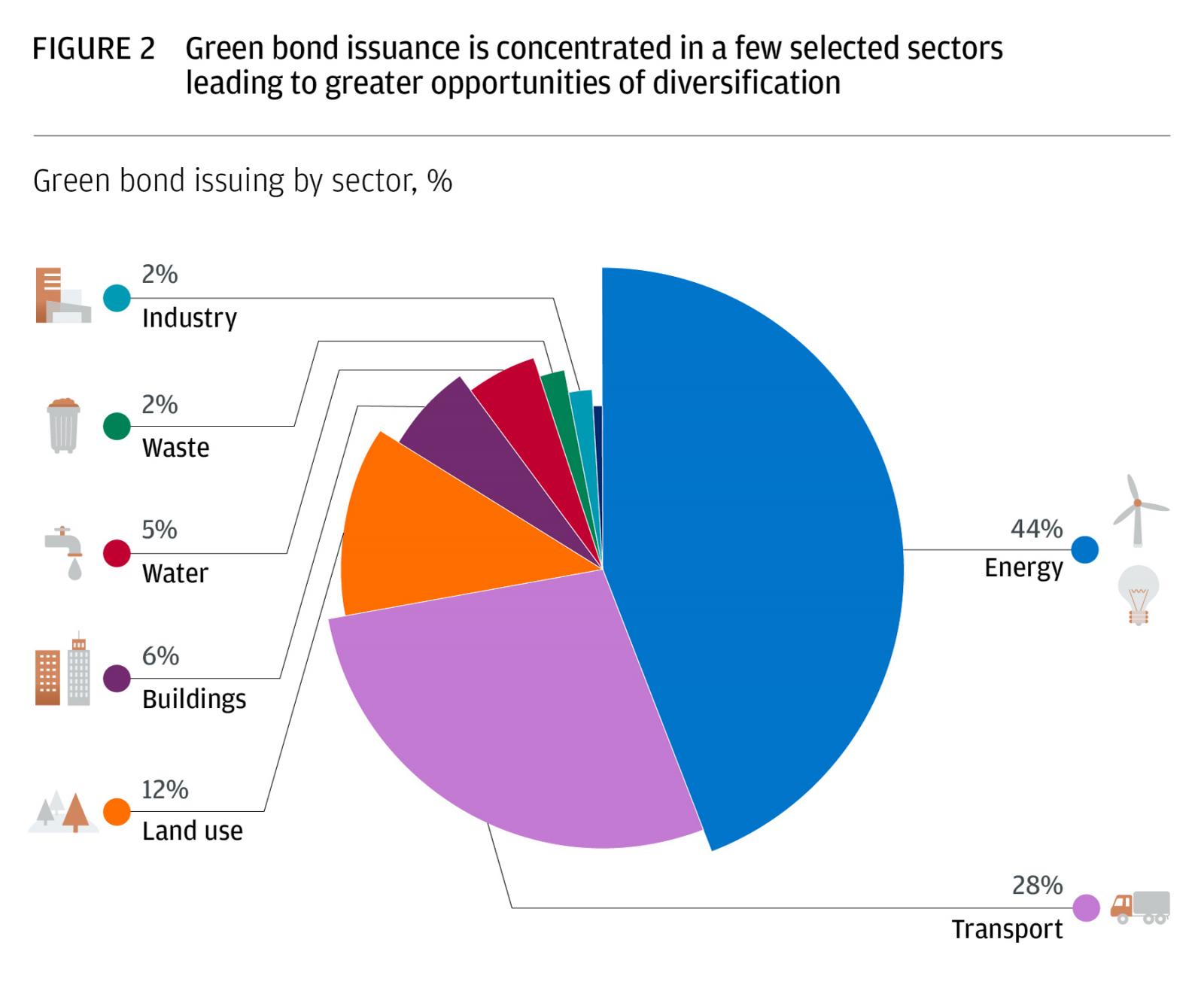

Major asset funds with ESG mandates, insurers and pension funds are contributing to the growth of burgeoning green bond market in the region. Green bonds, which are debt instruments created to fund projects that have positive environmental and/or climate benefits, have become a cornerstone of environmental, social and governance (ESG) investment. Issuance of green bonds in Latin America more than doubled in less than two years—from US$13.6bn in September 2019 to US$30.2bn at the end of June 2021.10 Half of these funds are dedicated to renewable energy projects (mainly solar and wind).

Brazil is the region’s largest green bond market, with US$10.3bn in cumulative issuance, followed by Chile (US$9.5bn) and Mexico (US$4bn). Several new countries have entered the green bond market over the past two years—Barbados, Bermuda, Ecuador and Panama—bringing the total number of green issuer countries in Latin America and the Caribbean (LAC) to 14.11 However, the market is still nascent. LAC only contributes to 2% of global green bond issuance, compared with 40% from Europe.12

While energy is the most funded sector in the green bond market, there are several other industries that present opportunities in the net-zero economy, including transport and land use (see Figure 2). In Chile, for example, most of the recently issued government bonds are for green transport, including Santiago’s Metropolitan Public Transport System’s new Metro subway lines.13 Land use, a significantly underfunded sector globally, represents over 10% of LAC issuance. The majority of these bonds fund certified agriculture, forestry and paper-related projects, especially from Brazil. However, there are other important sectors that remain unexplored. Buildings and water, two of the most funded sectors globally, are among the most lacking categories in Latin America.14

The Rise of Low-Emission Industries Creates New Opportunities for Investment in the Region

Shifts in energy demand could also impact the agricultural sector, as biofuels are quickly becoming a high-growth sector. A report on the region’s demand for biofuels illustrates this trajectory. While exports of basic agricultural products from Latin America, such as vegetable oil, sugar and cereals, grew at annual rates below 4.5% in the last decade, the bio-based sectors with the highest added-value—biofuels, bioplastics and biofertilisers, grew on average 25%, 20% and 14% annually in the past five years, respectively.16

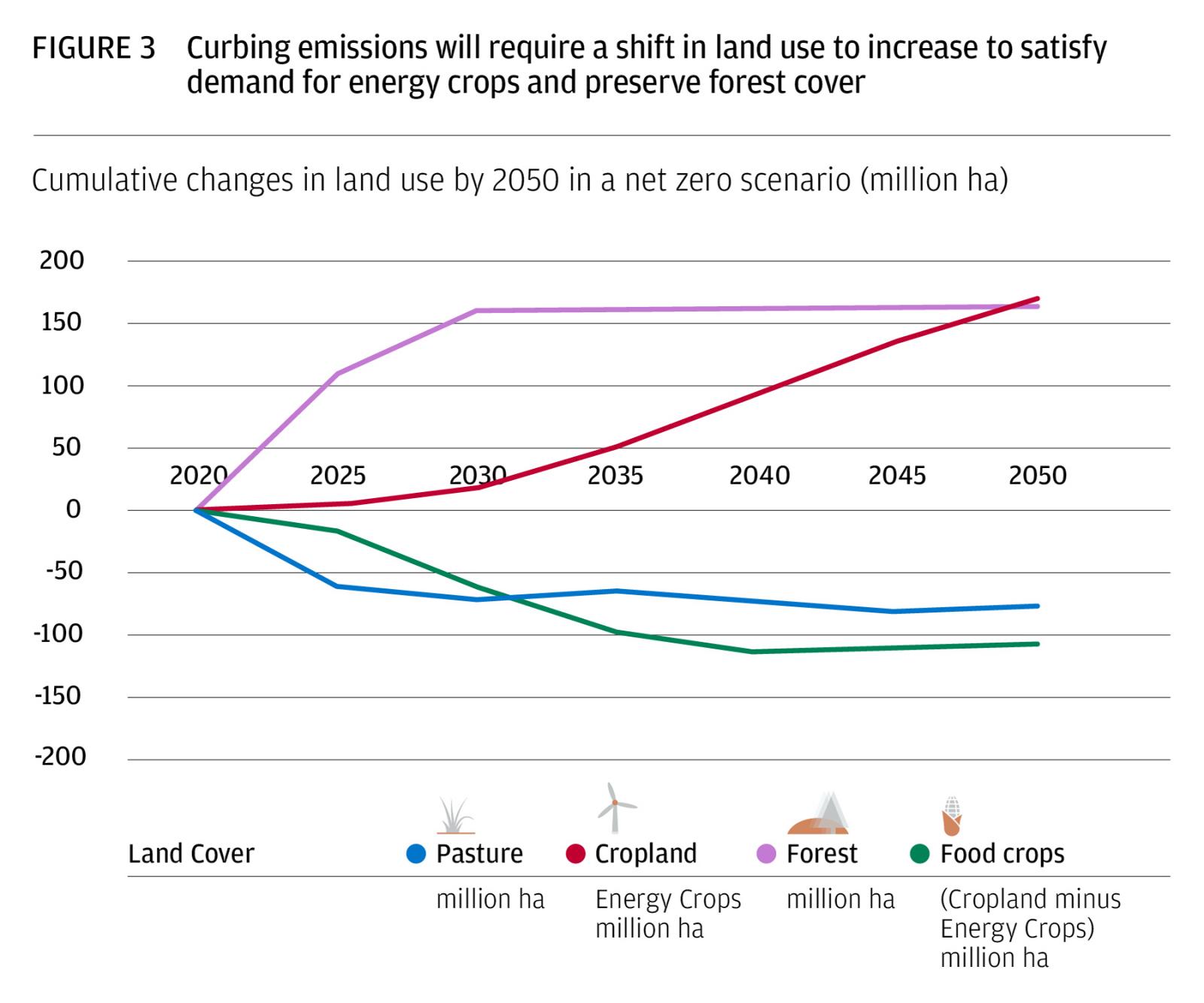

Increasing demand for biofuels might lead farmers to reduce cropland for food production and pasture land to give space to these profitable crops (see Figure 3).18 In order to maintain food production, the region would have to invest in sustainable agriculture to enhance crop yields, address food waste and food traceability, and adapt technology to livestock farming.19

New agricultural technologies (AgTech) could address a variety of problems across the sector, including new production systems, crop and animal protection and genetics, and food processing, logistics and distribution. AgTech also represents one of the most promising sectors for investors. In the United States, farm tech investing soared to US$7.9bn in 2020, topping 2019 investments by US$2.3bn, or 41%.20 Within this, agricultural biotech companies attracted particular interest from investors, with 173 deals closed, up by 58%.

This sector has remained under the radar for Latin American investors, but the region would greatly benefit as one of the world’s largest agricultural producers.21 Data from the Association for Private Capital Investment in Latin America show that there was US$35.4m in venture capital invested in AgTech across 15 disclosed rounds last year. The largest of these went to Colombia-based Frubana, a US$25m Series A round in early 2020.22 However, there are over 450 startups in the region’s AgTech sector. Most of these are concentrated in Brazil (51%), Argentina (23%) and the Andean Region (18%), which are also some of the food baskets of the region. These startups are concentrated in the development of local solutions in areas such as big data and precision agriculture, management software, and platforms for buying and selling services and funding.

Latin America’s Sequestration Potential Positions it as a Leader in the Carbon Credit Market

In addition to clean energy, demand for carbon offsets could impact land-use distribution in the region, as the value of forests increases due to their carbon sequestration potential. Carbon sinks are areas that store more CO2 than they release, and Latin America is home to one of the few remaining net carbon sinks in the world: the Amazon Basin, which stretches across eight countries23 and removes 1.2 Gt of CO2 a year.24

This is only part of the region’s potential. By simply allowing established forests to grow for another 40 years, Latin America would be able to potentially absorb up to 31 billion tons of CO2 out of the atmosphere—equivalent to the total carbon emissions from fossil fuel use and industrial processes in all of LAC from 1993 to 2014.25,26

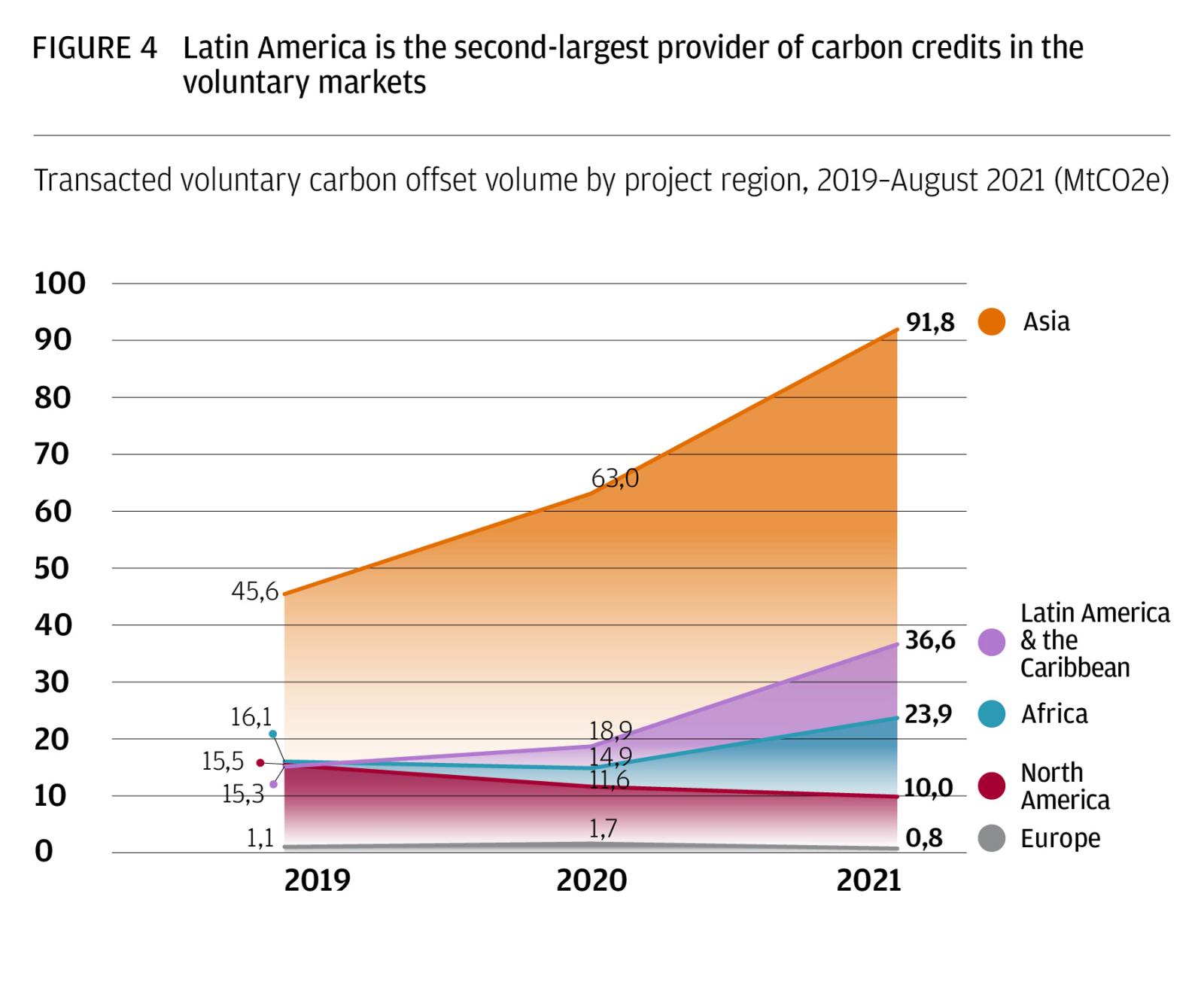

The region’s large carbon sequestration potential has led it to becoming the world’s second-largest provider of voluntary carbon credits, with just fewer than 20% of the total global credit supply coming from the region in 2020–21 (see Figure 4).

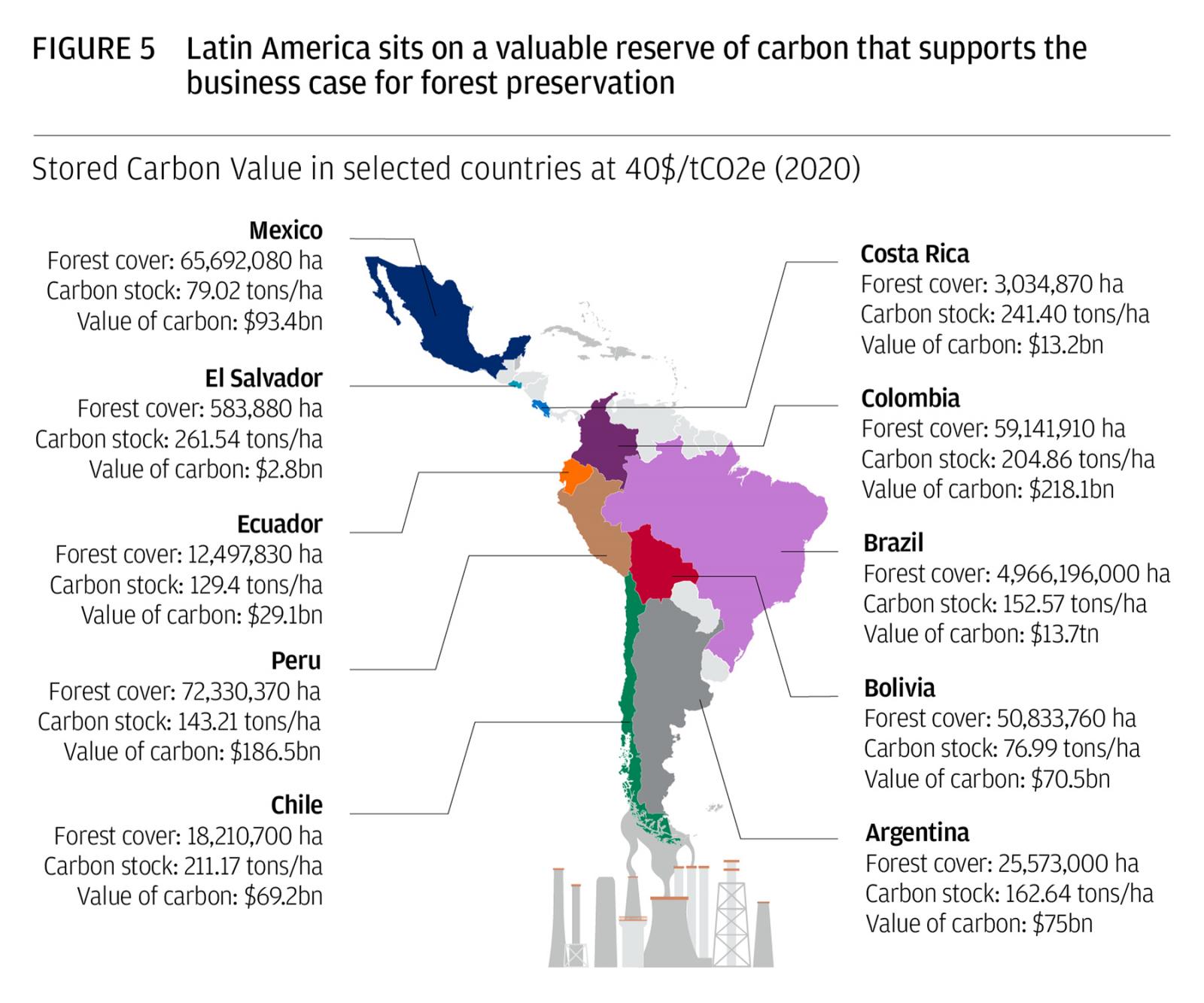

Latin American countries are sitting on some of the most valuable carbon deposits in the world. The total carbon stock of the region amounts to over 3.9 trillion tonnes, with a value of over US$14.5trn based on the 40$/tCO2e set in the Paris Agreement. At this price level, the value of Brazil’s carbon stock amounts to tenfold its current GDP, while Bolivia’s carbon value is twofold and Colombia’s 80% (see Figure 5).

Conclusion: A Network Effect Toward Net-Zero

Climate change represents an existential threat and, if left unaddressed, will have devastating environmental and economic impacts in Latin America. However, the transition to a net-zero economy also represents an opportunity for investors looking for long-term returns. The changes in demand from high-emitting goods and services to low-carbon alternatives could have a network effect that shifts resources from one industry to the other. Demand for low-carbon energy sources will affect not only the energy sector, but might also cascade into agriculture and land-use considerations. Other sustainable alternatives might have similar effects on a variety of industries, from waste management to water conservation. Investors who are able to anticipate these effects and make strategic investments will be able to reap the rewards.

1 Morningstar (2022) “Sustainable funds landscape report.” https://www.morningstar.com/lp/sustainable-funds-landscape-report

2 EU-LAC Foundation (2020), “The potential of the Green Bond markets in Latin America and the Caribbean.” https://repository.eafit.edu.co/bitstream/handle/10784/24798/the_potential_of_the_green_bond_markets_in_latin_america_and_the_caribbean_con_vinculos_a_instituciones.pdf?sequence=2&isAllowed=y

3 McKinsey (2022), “The economic transformation: What would change in the net-zero transition.” https://www.mckinsey.com/business-functions/sustainability/our-insights/the-economic-transformation-what-would-change-in-the-net-zero-transition

4 Tania Miranda, “NDCs in the Americas: A Comparative Hemispheric Analysis,” Institute of the Americas, 2019. https://user-9sjqssx.cld.bz/Nationally-Determined-Contributions-Across-the-Americas/11/

5 McKinsey (2022), “The economic transformation: What would change in the net-zero transition.” https://www.mckinsey.com/business-functions/sustainability/our-insights/the-economic-transformation-what-would-change-in-the-net-zero-transition

6 Oil rents are the difference between the value of crude oil production at regional prices and total costs of production.

7 World Bank (2021), “World Development Indicators.” https://data.worldbank.org/indicator/NY.GDP.PETR.RT.ZS

8 Bloomberg (2021), “Renewables Surge as Putin’s War Fuels Flight to Alternatives.” https://news.bloomberglaw.com/environment-and-energy/renewables-surge-as-putins-war-fuels-flight-to-alternatives?utm_source=rss&utm_medium=NEVE&utm_campaign=0000017f-2d83-d679-af7f-6db779220003

9 International Finance Corporation (2016), “Climate-Smart Investment Potential in Latin America: A Trillion Dollar Opportunity.” https://www.ifc.org/wps/wcm/connect/3e794608-cc7d-4499-9b6f-5342d7b6ddbc/LAC+1Trillion+6-13-16+web+FINAL.pdf?MOD=AJPERES&CVID=lmsI-Rx

10 Climate Bonds Initiative (2020), “Latin America & Caribbean: State of the Market.” https://www.climatebonds.net/files/reports/cbi_lac_2020_04e.pdf

11 Ibid.

12 EU-LAC Foundation (2020), “The potential of the Green Bond markets in Latin America and the Caribbean.” https://repository.eafit.edu.co/bitstream/handle/10784/24798/the_potential_of_the_green_bond_markets_in_latin_america_and_the_caribbean_con_vinculos_a_instituciones.pdf?sequence=2&isAllowed=y

13 Invest Chile (2020) Green bonds: Chile has allocated 24.8% of the US$2,373 million. https://blog.investchile.gob.cl/chile-has-already-allocated-24.8-of-the-us2373-million-issued-in-green-bonds-in-2019

14 Climate Bonds Initiative (2019), “Latin America & Caribbean: State of the Market.” https://www.climatebonds.net/files/reports/cbi_lac_sotm_19_web_02.pdf

15 Climate Bonds Initiative (2020), “Latin America & Caribbean: State of the Market.” https://www.climatebonds.net/files/reports/cbi_lac_2020_04e.pdf

16 UN Economic Commission for Latin America and the Caribbean (2020), “The Outlook for Agriculture and Rural Development in the Americas: A Perspective on Latin America and the Caribbean 2021–2022(ECLAC).” https://repositorio.cepal.org/bitstream/handle/11362/47209/1/ECLAC-FAO21-22_en.pdf

17 Network for Greening the Financial System (2021), “NGFS Climate Scenarios for central banks and supervisors.” https://www.ngfs.net/sites/default/files/media/2021/08/27/ngfs_climate_scenarios_phase2_june2021.pdf

18 Ibid.

19 Fabian Gosselin (2021), “AgTech Innovation and Investment Opportunities in Latin America.” https://www.supplychangecapital.fund/blog2/agtech-innovation-and-investment-opportunities-in-latin-america

20 Louisa Burwood-Taylor (2021), “Farm Tech Investing Is Accelerating Faster Than Food Tech and General VC—New Report,” Forbes. https://www.forbes.com/sites/louisaburwoodtaylor/2021/07/29/farm-tech-investing-is-accelerating-faster-than-food-tech-and-general-vcnew-report/?sh=6dd9f8874cf0

21 Ibid.

22 Isabella Fleichsman, “Which startup will be the first LatAm agtech unicorn?” https://labsnews.com/en/articles/business/which-startup-will-be-the-first-latam-agtech-unicorn/

23 Bolivia, Brazil, Colombia, Ecuador, Guyana, Peru, Suriname and Venezuela.

24 Nancy Harris and David Gibbs (2021) “Forests Absorb Twice as Much Carbon as They Emit Each Year,” World Resources Institute. https://www.wri.org/insights/forests-absorb-twice-much-carbon-they-emit-each-year

25 Justin Gillis (2016), “In Latin America, Forests May Rise to Challenge of Carbon Dioxide,” The New York Times. https://www.nytimes.com/2016/05/17/science/forests-carbon-dioxide.html

26 Robin Chazdon, Eben Broadbent, Danaȅ Rozendaal, et al. (2016), “Carbon sequestration potential of second-growth forest regeneration in the Latin American tropics,” Science Advances, May 13, 2016. https://www.science.org/doi/10.1126/sciadv.1501639

27 Stephen Donofrio, Patrick Maguire, Kim Myers (2021), “Buyers of Voluntary Carbon Offsets, a Regional Analysis.” https://app.hubspot.com/documents/3298623/view/125182374?accessId=a759f9

28 Ecosystem Marketplace (2021), “EM Data Intelligence & Analytics Dashboard.” https://data.ecosystemmarketplace.com/

29 Stephen Donofrio, Patrick Maguire, Kim Myers (2021), “Buyers of Voluntary Carbon Offsets, a Regional Analysis.” https://app.hubspot.com/documents/3298623/view/125182374?accessId=a759f9; Ecosystem Marketplace, EM Data Intelligence & Analytics Dashboard, updated December 2, 2021.

30 Ecosystem Marketplace (2021), “EM Data Intelligence & Analytics Dashboard.” https://data.ecosystemmarketplace.com/

31 FAO (2020), “Global Forest Resource Assessment.” https://fra-data.fao.org/